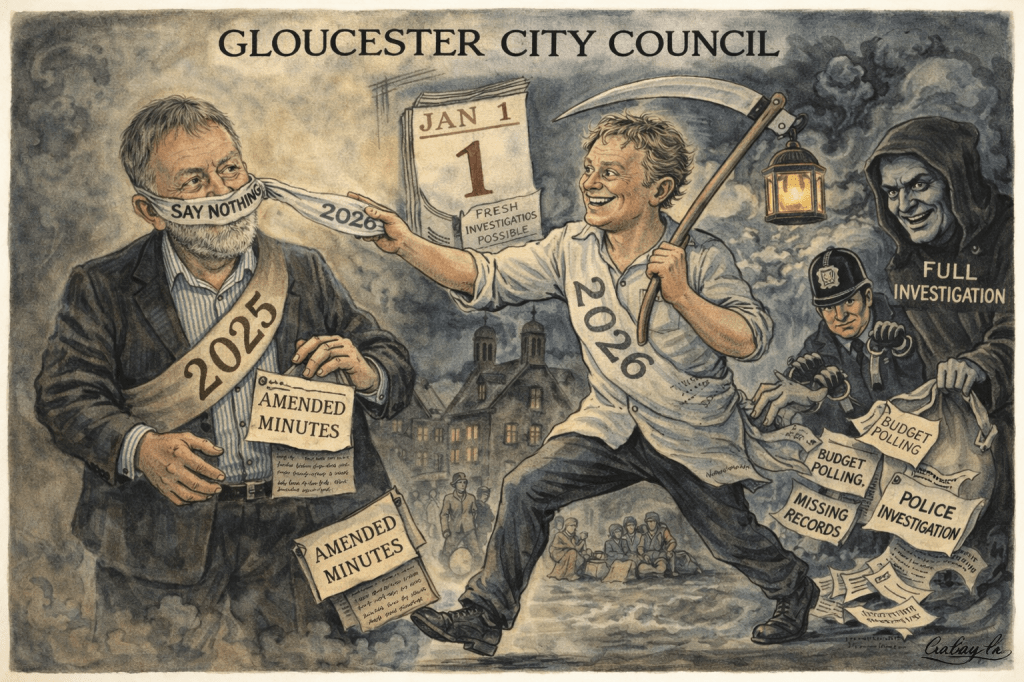

On Monday 5 January 2026 at 6:30 pm, Gloucester City Council’s Overview and Scrutiny Committee meets under a cloud it did not create, but must now confront.

A £17.5 million hole in the Council’s finances has emerged not as a sudden shock, but as the end result of decisions, warnings, and controls that either failed or were ignored. How and when senior officers became aware of the looming deficit, why it was not escalated sooner, and how official records potentially came to be amended and obscured rather than clarified are no longer technical questions, they are matters of public trust.

The questions that follow are not political point-scoring, nor are they unreasonable. They are the minimum that any responsible scrutiny body should be asking if it is to demonstrate independence, restore confidence, and show that those who may be examined are not also deciding which questions are allowed to be asked.

Proposed Questions for Overview & Scrutiny – Gloucester City Council

1. Timing, Knowledge, and Disclosure of the Deficit

On what exact date was it first identified by senior officers that Gloucester City Council was likely to face a serious and material budget deficit?

At what point did this risk move from being a forecast concern to a known and unavoidable financial shortfall?

Once that threshold was crossed, who was informed, when, and by what formal mechanism (Cabinet briefing, written report, risk register update, or otherwise)?

Can the Committee confirm whether all councillors were informed at the same time, and if not, why not?

2. KPI Monitoring, Budgetary Controls, and Early Warning Systems

What Key Performance Indicators (KPIs) were used to measure financial performance against approved budgets during the period in question?

Were these KPIs reviewed monthly, quarterly, or at another interval, and where is the documentary evidence of those reviews?

If KPIs were being monitored appropriately, how did a £17.5 million deficit develop without triggering earlier intervention or escalation?

If KPIs were not being monitored with sufficient frequency or rigour, does the Council accept that this represents a systemic failure of financial governance?

3. Accuracy, Integrity, and Amendment of Minutes

Can the Committee confirm whether meeting minutes were amended after the event in ways that materially altered the record of concerns raised, warnings given, or decisions taken?

What governance safeguards exist to prevent retrospective alteration of the official record, and were those safeguards followed in this case?

Were any amendments made without explicit committee approval, and if so, who authorised them?

4. Financial Propriety and Officer Accountability

Given the seriousness of the deficit and the questions surrounding disclosure and record-keeping, does the Committee accept that there are credible concerns relating to financial propriety and candour at senior officer level?

In light of those concerns, how does the Committee justify allowing senior officers who may be subject to scrutiny or investigation to act as gatekeepers of public and member questions?

5. Conflict of Interest and Gatekeeping of Scrutiny

Does the Committee accept that it is constitutionally improper and procedurally unsafe for individuals who may be investigated to:

determine which questions are admissible,

edit or reframe those questions, or

exclude lines of inquiry relating to their own actions?

What independent safeguards exist to prevent conflicts of interest in the handling of scrutiny questions—and why were they not used here?

6. Free Speech, Democratic Scrutiny, and Procedural Legitimacy

Does the Committee believe that current Gloucester City Council procedures unduly restrict democratic scrutiny, particularly where questions relate to officer conduct, governance failures, or statutory duties?

How does the Council reconcile its approach with the principles of openness, accountability, and freedom of political expression expected of a local authority?

Will the Committee commit to reviewing the legitimacy of procedures that effectively censor questioning under the guise of admissibility, brevity, or officer discretion?

7. Independent Review

Finally, given the scale of the financial failure and the procedural concerns raised, does the Committee support:

an independent governance review, and/or

the involvement of an external auditor or investigator

to restore public confidence?