To: Councillor Caroline Courtney, Cabinet Member for Culture and Leisure

Councillor Jeremy Hilton, Leader of Gloucester City Council

Phil Hindson, Chief Executive of Gloucester Culture Trust

Members of Gloucester City Council’s Cabinet and the trustees of Gloucester Culture Trust

Subject: Gloucester’s proposed UK City of Culture bid — putting Gloucester’s culture first

Dear Councillor Courtney, Councillor Hilton, Mr Hindson and colleagues,

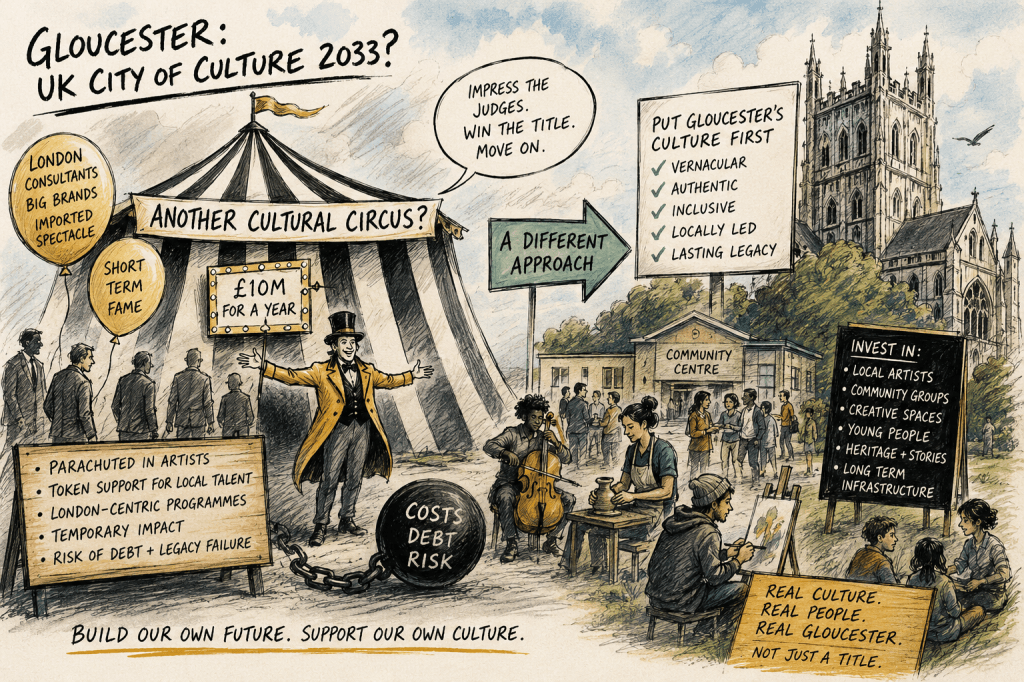

I am writing following the decision to include a possible bid for UK City of Culture 2033 within Gloucester’s new ten-year Cultural Strategy.

Let me begin by saying that I share the ambition to promote Gloucester and strengthen its cultural life. Gloucester is not short of culture, creativity, history or talent. The important question, however, is whether entering the UK City of Culture competition is the most effective way of supporting those assets—or whether the considerable resources required to prepare and promote a bid would achieve more if invested directly in Gloucester’s existing artists, performers, venues and community organisations.

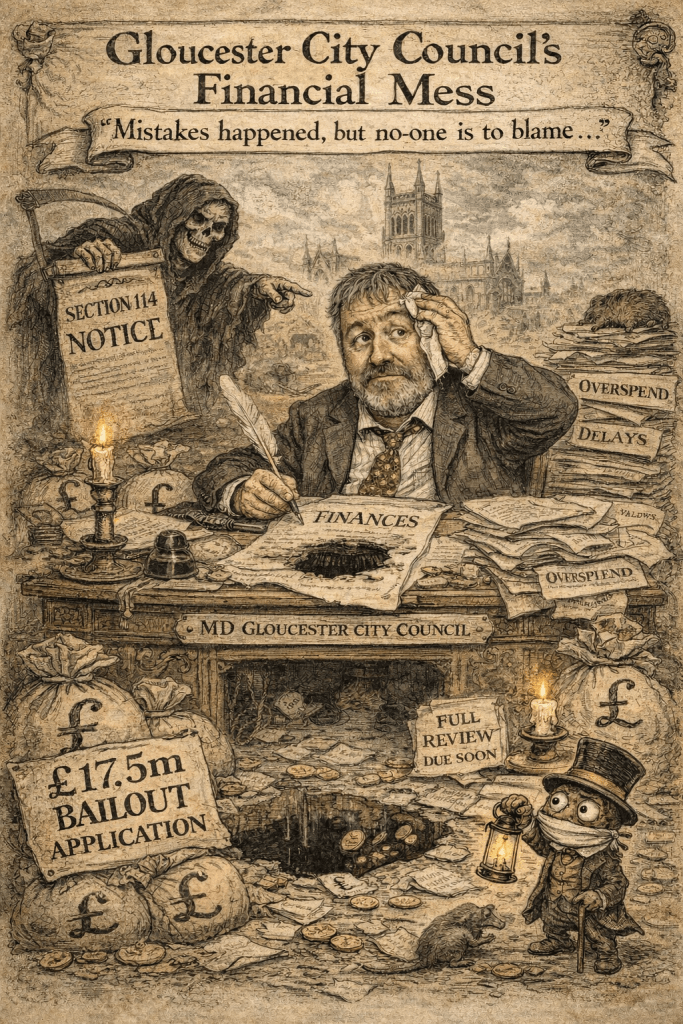

This distinction matters particularly in the present financial circumstances. Gloucester City Council’s own budget report said that it was seeking Exceptional Financial Support, needed approximately £1 million in savings during 2026/27, was reducing support for festivals and events, cutting the Museum of Gloucester’s opening days, ending a small discretionary grants scheme and imposing strict limits on discretionary spending.

Against that background, residents are entitled to know precisely how much a City of Culture bid would cost—not only in cash payments to consultants, producers, branding agencies and bid writers, but also in officer time and the displacement of other work.

The Government’s own recent evidence review presents positive headline results from previous titleholders, including increased participation, civic pride, tourism and cultural investment. Those successes should be acknowledged. However, the same review records that shortlisted places have spent between £50,000 and £1.5 million merely bidding. It also accepts that attribution of economic benefits can be challenged, that evaluation methods have varied and that only Coventry had undertaken a full social cost-benefit and value-for-money assessment.

There are also lessons about governance and financial risk. Coventry’s year undoubtedly produced successful projects and investment, but the Coventry City of Culture Trust subsequently entered administration. Coventry City Council reported that it was owed approximately £1.677 million, including an unpaid loan and other services. Gloucester must learn from both the achievements and the failures of previous titleholders.

My greatest concern is that Gloucester should not become host to another temporary cultural circus: an impressive procession of outside consultants, nationally recognised artistic directors and imported productions that arrives with great fanfare, uses local people principally as volunteers or supporting players, and then moves on to the next city.

Too often, major cultural programmes appear to be created around a metropolitan—or essentially London-centric—understanding of what constitutes worthwhile culture. Local communities can then find themselves presented with an externally designed programme intended to satisfy funding bodies, cultural institutions and judging panels rather than one growing naturally from the identity of the place.

Gloucester must not be encouraged to imitate somebody else’s idea of a cultural city.

Its culture is vernacular. It is found in its neighbourhoods, schools, churches, community centres, workshops, pubs, rehearsal spaces, theatres, festivals, sporting traditions and voluntary organisations. It is expressed through its cathedral and historic buildings, its docks and industrial inheritance, its music, theatre, visual arts, diverse communities and the stories of ordinary Gloucester people. This culture already exists. The task should be to nourish it, connect it and provide the people creating it with sustainable opportunities.

In my earlier article, Addressing the Shortcomings of the UK City of Culture Initiative: Toward a More Inclusive and Locally-Driven Model, I argued that cultural regeneration should be built around local control, representative governance, investment in permanent capacity and a broad definition of culture—not the parachuting-in of experts carrying a generic programme from one city to another.

The council’s new Cultural Strategy itself promises to strengthen Gloucester’s cultural ecosystem, support local artists, develop infrastructure and enable residents to shape cultural activity. Those are welcome commitments. The proposed City of Culture bid should therefore be tested against them, rather than being allowed to dominate or redirect them.

Before substantial resources are committed, I would ask the council and Gloucester Culture Trust to publish clear answers to the following questions:

What is the maximum amount of public money and officer time that could be committed to preparing the bid?

What locally delivered cultural activity could be funded with the same resources if Gloucester did not bid? There should be a published comparison between the bid and an alternative programme of direct grants, commissions, apprenticeships, venue support and artist development.

What proportion of the programme and commissioning budget would be guaranteed to Gloucester-based artists, performers, producers and cultural organisations? Local participation must mean more than volunteering, consultation or appearing within projects led and controlled from elsewhere.

Will a majority of the governing and decision-making body be people who live or work in Gloucester, including independent artists, performers, community organisations and residents who are not already part of the established cultural administration?

What would every external appointment or imported production leave behind? Outside expertise can be valuable, but it should transfer skills, build local capacity, mentor local practitioners and establish lasting partnerships rather than simply extracting fees.

How much investment would be directed toward permanent cultural infrastructure and long-term organisational capacity rather than temporary performances, publicity and spectacle?

What protections would prevent the council from assuming open-ended liabilities or rescuing a delivery organisation if income, sponsorship or ticket sales failed to meet expectations?

How would success be independently measured? Evaluation must distinguish genuinely additional activity from investment that was already planned, account for displacement from existing events and venues, and measure what remains five and ten years later.

The Government’s evidence review now specifically proposes tracking local-artist representation and career development, precisely because these matters have not been measured consistently across previous titleholders. Gloucester should make this a binding commitment from the beginning, not an aspiration considered after the programme has been designed.

I am not asking Gloucester to abandon ambition. I am asking that ambition be directed toward the people who already make the city culturally distinctive.

A successful cultural strategy should not be judged principally by whether Gloucester secures a national title in 2033. It should be judged by whether, in 2034 and beyond, more local artists can earn a living; more children can develop creative skills; more community organisations can obtain affordable space; more venues are secure; more residents participate; and Gloucester possesses stronger cultural institutions than it did before.

Please do not allow the title to become the objective while Gloucester’s actual culture becomes merely the raw material used to obtain it.

Should the council decide to proceed, it must be a Gloucester-led bid, not merely a bid located in Gloucester. Local artists and communities should control it, receive the greater part of its resources and inherit its lasting benefits.

Otherwise, the more courageous and culturally valuable decision may be to spend the money directly on Gloucester’s people and allow the city’s own culture to flourish without waiting for permission—or a title—from London.

Yours sincerely,

Jason I. J. Smith