A balance sheet recession occurs when the private sector is focused on paying down debt and unwilling to borrow and spend (despite zero interest rates). This reluctance to spend and invest causes a sustained weakness in aggregate demand and lower growth.

In a balance sheet recession the banking sector is unwilling to lend because it needs to improve its balance sheet and increase bank reserves.

A balance sheet recession also usually involves falling asset prices and deflationary pressures.

For example, in 1991, the UK experienced a recession caused by a demand side shock (high interest rates and strong pound). When interest rates were cut and the pound devalued, the economy was able to recover. However, in a balance sheet recession, the problem is more fundamental than a temporary demand side shock. This explains why when interest rates were cut in 2008, it failed to solve the recession – because firms, banks and consumers were trying to reduce exposure to debt and increase saving.

Other Features of Balance Sheet Recessions

- Liquidity trap – zero interest rates fail to boost spending or investment because firms and consumers can’t afford to borrow more despite the lower interest rates. (liquidity trap)

- Falling Asset prices – The reluctance to borrow means demand for mortgages and houses will fall. This leads to a sustained fall in asset prices. Falling asset prices tend to exacerbate bank losses, making banks even more reluctant to lend.

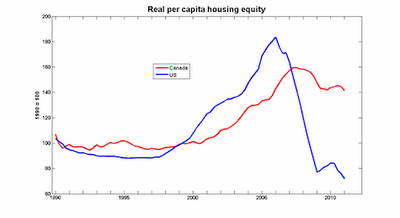

Graph showing the extent of how much house prices in the US have fallen since start of balance sheet recession. Source: Economists view

- Deflationary Pressure. The combination of falling asset prices and stagnant economy can lead to disinflation or actual deflation. Deflation increases the real value of debt and increases the pressure on firms to pay down debt rather than invest or spend.

- Higher saving rates.

Before the recession, saving rates fell to very low levels as borrowing increased. Following the start of the recession, saving rates increased in countries like Ireland, UK and US as consumers tried to pay off debts and increase savings.

- Low Bond Yields. Typically, higher government borrowing leads to higher interest rates (markets fear default). However, in a balance sheet recession, there is high demand for government bonds (because the private sector are risk averse and want to increase savings. Government bonds are seen as one of most relatively secure.

E.g. Japan had government sector debt of over 220% of GDP, yet bond yields were as low as 1%.

In 2011, The US has seen a fall in bond yields to 1.75% on 10 year treasury bonds, despite a rise in government borrowing.

Problems of Balance Sheet Recession

- Conventional monetary policy is insufficient to boost demand. Lower interest rates not enough to encourage spending and investment.

- Fall in private sector spending, creates shortage of demand.

- Negative multiplier effect. Unfortunately, falling asset prices leads to big debts for banks and a greater reluctance to spend.

- Deflation. A deflationary spiral discourages further spending and increases real value of debt.

- They can last a long time. e.g. Lost decade of Japan. Prospect of double dip recession in west and a long period of stagnant incomes, high unemployment and low growth.

- Scope for biflation (both commodity price inflation and deflation of other goods at same time)