Gloucestershire is edging toward a “Mass Rapid Transit” (MRT) bus corridor between Cheltenham and Gloucester. It is… something. But for two urban areas that should act as a genuine counterweight to Bristol and Birmingham, an express bus is not the transformative step our county needs. The corridor deserves an integrated, rail-anchored, transit-oriented plan that unlocks housing at scale, stitches the centres together, and builds a platform for future industries rather than simply speeding today’s commute. The prize is more jobs, higher productivity and a step-change in place quality. The risk of doing the minimum is more of the same.

On 29 October, county leaders proposed just £1.25 million to progress MRT design work — modest money for a modest concept.

A vision that matches the geography

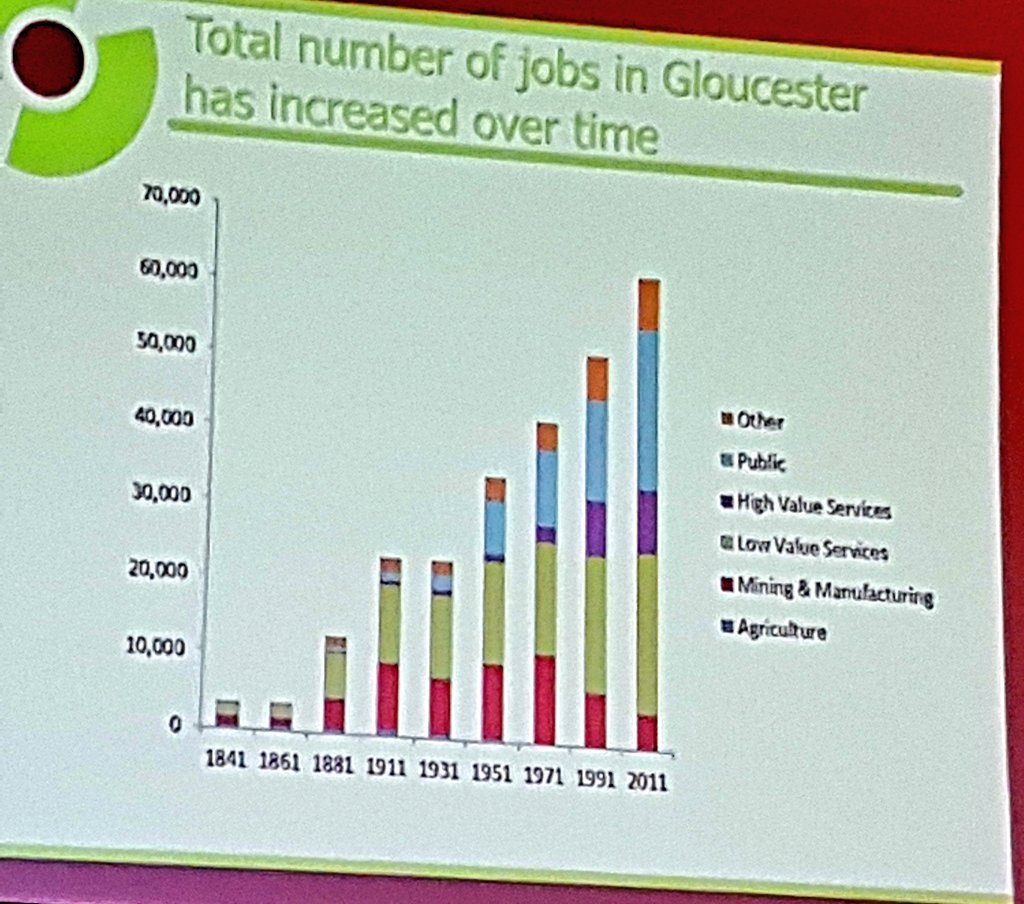

Cheltenham and Gloucester already function as a single labour market divided by the M5 and decades of piecemeal transport thinking. Official strategies admit rail connectivity is central to prosperity, yet we continue to default to buses on congested roads.

A credible alternative is on the table:

Re-activate the former rail alignment and run tram-train services centre-to-centre, interworking with the national network. This is not science fiction; the UK has already proved the tram-train model technically and operationally (Sheffield–Rotherham), along with the institutional lessons about standards, power, and signalling.

Add a station at Staverton (Gloucestershire Airport) and repurpose most of the airfield into a 20,000-home transit-oriented district, keeping a compact apron as a VTOL hub feeding BHX, BRS and LHR as advanced air mobility scales up. The county is already exploring new futures for the airport; the question is whether we aim high enough.

This is how you build a real counterweight: by hard-wiring people, jobs, education and culture together with rail, and by placing a major new community on that spine rather than scattering estates around rural junctions.

What the evidence says about rail-anchored growth

We don’t need to guess at the economic upside of modern light rail and tram-train. Multiple UK evaluations point the same way:

Light rail stimulates city economies and investment. The Knowles & Ferbrache synthesis for UKTram found consistent links to business location, private development, labour-market access and image effects across UK systems.

Manchester Metrolink has repeatedly been associated with improved access to jobs, education and healthcare and with development around stops; the “transformative impacts” literature used Metrolink as a UK case.

Nottingham NET Phase Two supported around 1,600 direct construction jobs at peak, with documented local skills and supply-chain programmes, an approach local authorities are urged to copy because it converts construction spend into local employment and capability.

Rail investment uplifts land value and drives new homes. Crossrail’s pre-opening studies estimated £20.1 bn of additional residential value and up to 180,000 homes in the pipeline; a separate assessment found a ~2.2% house-price uplift near stations over 2008–2019. While our scheme is smaller, the direction of travel is clear: high-quality rail capacity attracts development and raises values that can be recycled through land-value capture.

The Department for Transport’s own cross-case evaluation confirms rail can produce measurable productivity and employment impacts where it is integrated with local plans and laments the shortage of robust ex-post evaluation only because too many schemes were not designed to capture the benefits properly. We should learn from that and design for measurement and value capture from day one.

Why buses alone won’t do it

Bus Rapid Transit can be great for specific corridors, but it rarely generates the same permanence signal to investors. That “steel in the ground” matters: developers and institutions bank on fixed rail. Academic reviews consistently show light rail’s place-making effects, the image, certainty and clustering that pull in private capital, outpacing bus-only schemes when cities are competing for talent and firms.

Housing at scale — on the transit spine, not on the bypass

Gloucestershire needs homes and good ones. Industry-standard multipliers suggest each new dwelling supports ~2.4–3.4 total jobs (direct, indirect, induced) during build-out, varying by product mix. On 20,000 homes, that’s on the order of 48,000–68,000 job-years over the programme, plus ongoing local services employment once occupied. Pair that with a rail station at the heart of the district and you have a liveable, low-carbon growth pole rather than a traffic problem.

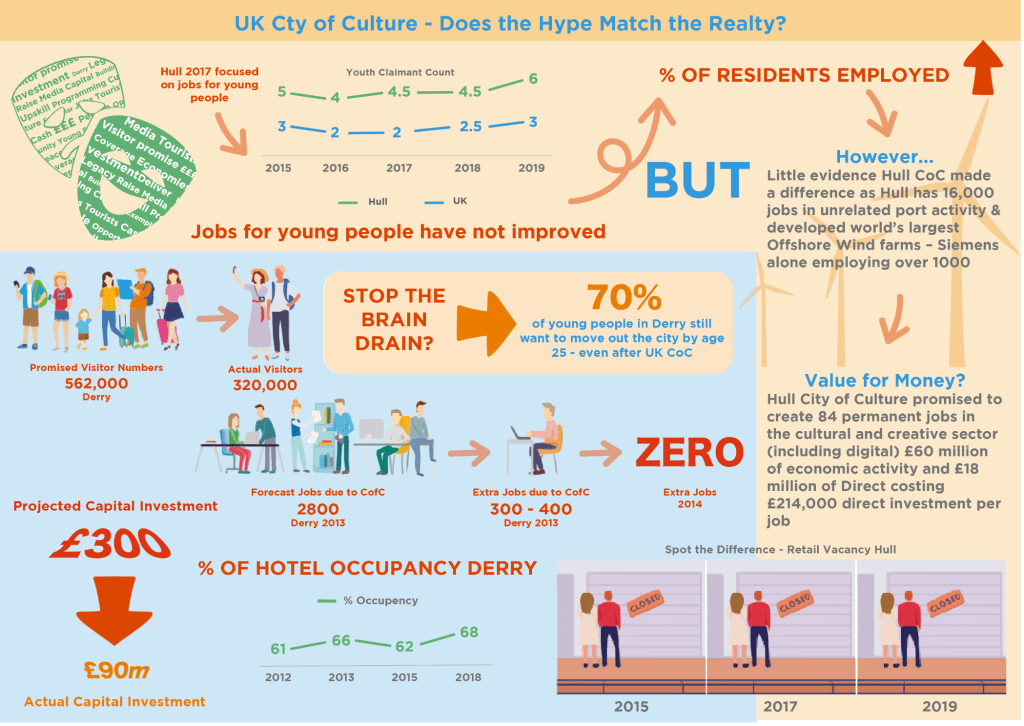

Internationally, airport-to-urban conversions often anchor research, advanced manufacturing and housing (cf. Berlin Tegel’s “Urban Tech Republic”, though Berlin’s slow delivery is a warning to govern and finance these projects competently). The UK government has even commissioned frameworks for understanding airport-economy links, useful both for strengthening the VTOL hub business case and for judging alternatives to conventional aviation land-use.

A realistic take on risks (and how to manage them)

Costs and delivery: The Sheffield tram-train pilot suffered a notorious cost overrun; we should treat that as a lesson in governance and standards, not a veto on the model. Package the scheme with clear risk-allocation, early utilities coordination, and a funding stack that blends local land-value capture with central grants.

Planning and capacity: The national planning system is short of case officers; phasing and a dedicated delivery vehicle will be essential to avoid the bottlenecks now stalling UK housing output.

Airport transition: If we retain a compact apron for VTOL and training while releasing most land for housing, we must evidence net economic gain versus status-quo aviation. The DfT local airport-economy framework gives us the methodology.

What success looks like (and what it’s worth)

In practical terms, a Cheltenham–Gloucester tram-train with a Staverton station + 20,000-home TOD could deliver:

Construction employment: ~48k–68k job-years over build-out, with targeted apprenticeships and local procurement (copy NET’s model).

Productivity uplift: accelerated access to GCHQ/Cyber Park, the hospitals, colleges and major employers, the same access-to-opportunity effects documented for Metrolink and other UK light-rail systems.

Land-value and fiscal gains: material property-value uplift near stations and a pipeline of private development that can be hypothecated to repay core infrastructure (Crossrail provides the clearest UK precedent for value capture at scale).

Place quality and investment narrative: light rail’s durable “place-signal” is repeatedly cited as a factor in attracting employers and investment, the sort of intangible that becomes very tangible in site decisions.

The choice in front of us

Cheltenham grew just 2.7% between 2011 and 2021; Gloucester grew 8.9%. Together they could , and should, behave like a single mid-sized city with the heft to keep graduates, attract firms and share prosperity more evenly. Doing that with a bus lane is unlikely. Doing it with rail-anchored transit and a new urban district at Staverton is bold, evidence-led and financeable if we capture the uplift we create.

Gloucestershire has been talking about growth for a decade. The strategic plans say connectivity drives prosperity. It’s time to believe our own strategies, and to act accordingly.

Notes: Key sources include UKTram/academic evaluations of light rail impacts; DfT case studies on rail investment; Crossrail value-uplift studies; HBF employment multipliers for housing; Nottingham NET and Metrolink evidence; Gloucestershire strategies; and current reporting on the MRT proposal and Gloucestershire Airport’s future.

The Fastershire project is seeking the services of a suitably qualified consultant to help crystallise an understanding of the need, demand, opportunity, and potential for pervasive full fibre connectivity within the urban localities of Gloucestershire. The study will need to identify the needs of and available infrastructure assets owned by public sector partners including local councils, the NHS and emergency services as well as the education sector. Additionally it will need to investigate and assess the appetite of various private sector organisations to leverage the demand and assets of the public sector to generate full fibre connectivity more widely. In the first instance to key business parks, regeneration zones, GPs Surgeries and student accommodation but potentially further providing all pervasive residential and business access to full fibre access across the Study Area.

The Fastershire project is seeking the services of a suitably qualified consultant to help crystallise an understanding of the need, demand, opportunity, and potential for pervasive full fibre connectivity within the urban localities of Gloucestershire. The study will need to identify the needs of and available infrastructure assets owned by public sector partners including local councils, the NHS and emergency services as well as the education sector. Additionally it will need to investigate and assess the appetite of various private sector organisations to leverage the demand and assets of the public sector to generate full fibre connectivity more widely. In the first instance to key business parks, regeneration zones, GPs Surgeries and student accommodation but potentially further providing all pervasive residential and business access to full fibre access across the Study Area.